Investment Thesis: JD.com (JD)

Chinese E-commerce bet with a margin of safety.

Overview

JD is a Chinese ecommerce company competing with Alibaba and Pinduoduo. They are operating a 1P business model where the majority of their revenue comes from selling goods directly to consumers, this gives them more operational control but requires much capital and heavy investments in assets. They have 3 core business segments: JD Retail 83.47% of revenue, JD logistic 14.89% of revenue and New Businesses 1.64% of revenue. JD Retail produces a 4.00% operating margin, JD Logistic 2.80% and New Businesses operates on a loss of (14.40%). JD Retail accounts for the majority of the revenue and profit. They sell everything from gaming computers, phones, household items, jackets etc. Their focus is to provide quality goods with low shipping time and great customer service. Although JD Logistic is not as profitable as the retail segment, it contributes to the success of the retail segment by offering superb logistic service which in turn benefits the retail segment, so the logistic segment is much more valuable to JD than what the books show. New Businesses consist of unicorn projects.

Due to decreased consumer spending in China and increased competition, JD.com has experienced stagnated growth. From 2021 the share price have plunged around 75%. However, JD.com has improved its business structure by reducing costs and increasing gross margin and free cash flow, while also expanding its infrastructure. Given JD.com's great infrastructure and position as a premium supplier, I believe it will benefit once the Chinese economy regains momentum again.

Moat analysis

Over the last 20 years, JD.com has aggressively invested in logistics, and I believe their investments have created a moat that is very hard to come by. JD.com’s logistics network consists of: 75 000 trucks, 2 000 cloud warehouses, 1 600 warehouses and 350 000 in-house delivery personnel; An asset heavy business model to say the least. This infrastructure enables JD.com to deliver orders placed before 11:00 AM the same day, and orders placed after 11:00 PM the following day reaching nearly every corner in China. JD is a clear leader in logistic in China compared to their competitors. As of 2022, Alibaba’s logistics company Cainiao can provide same-day or next-day delivery to 1,500 districts and counties, compared to JD.com, which had already achieved this capability in 1,752 counties and districts by 2017. According to JD Logistics' 2021 report, they achieved same-day or next-day deliveries in 93% of counties and 84% of towns and villages in China. A study also shows that JD ranks number one as the platform with the highest reliability in logistics time efficiency in China. JD also have quicker or similar inventory turnover versus global peers. JD's inventory turnover days is 25.74 in 2024, which is similar to Amazon’s 24.88 but lower than Costco’s 30.76. Walmart had an inventory turnover of 39.93.

Capital-intensive businesses usually have lower margins. But it’s important for investors to understand the rationale behind the high capital intensity. In JD’s case, I believe their capital-intensive business model is a clear strength. It enables them to offer better shipping time and product quality to their customers, which have established them as more trusted retailer than that of competitors. JD’s logistics operations are highly complex and labor-intensive, requiring an enormous amount of capital investment. I believe it is reasonable to say that building their logistic infrastructure from scratch would take around 20 years. One could argue that there are more resources available to quicker and more effectively build logistic infrastructure now than in the early 2000. One should consider that JD just recently started making profit and a business model like this operates on very thin margins. You not only have to get access to huge amounts of capital, but you also have to convince investors to keep giving you money even though you will operate on a net loss for the first 10-15 years. JD is so long ahead of the game compared to their competitors that it is very hard for them to catch up. JD is also integrating AI solutions to streamline their operations even further, they have for example created the first fully automated warehouse located in Shanghai.

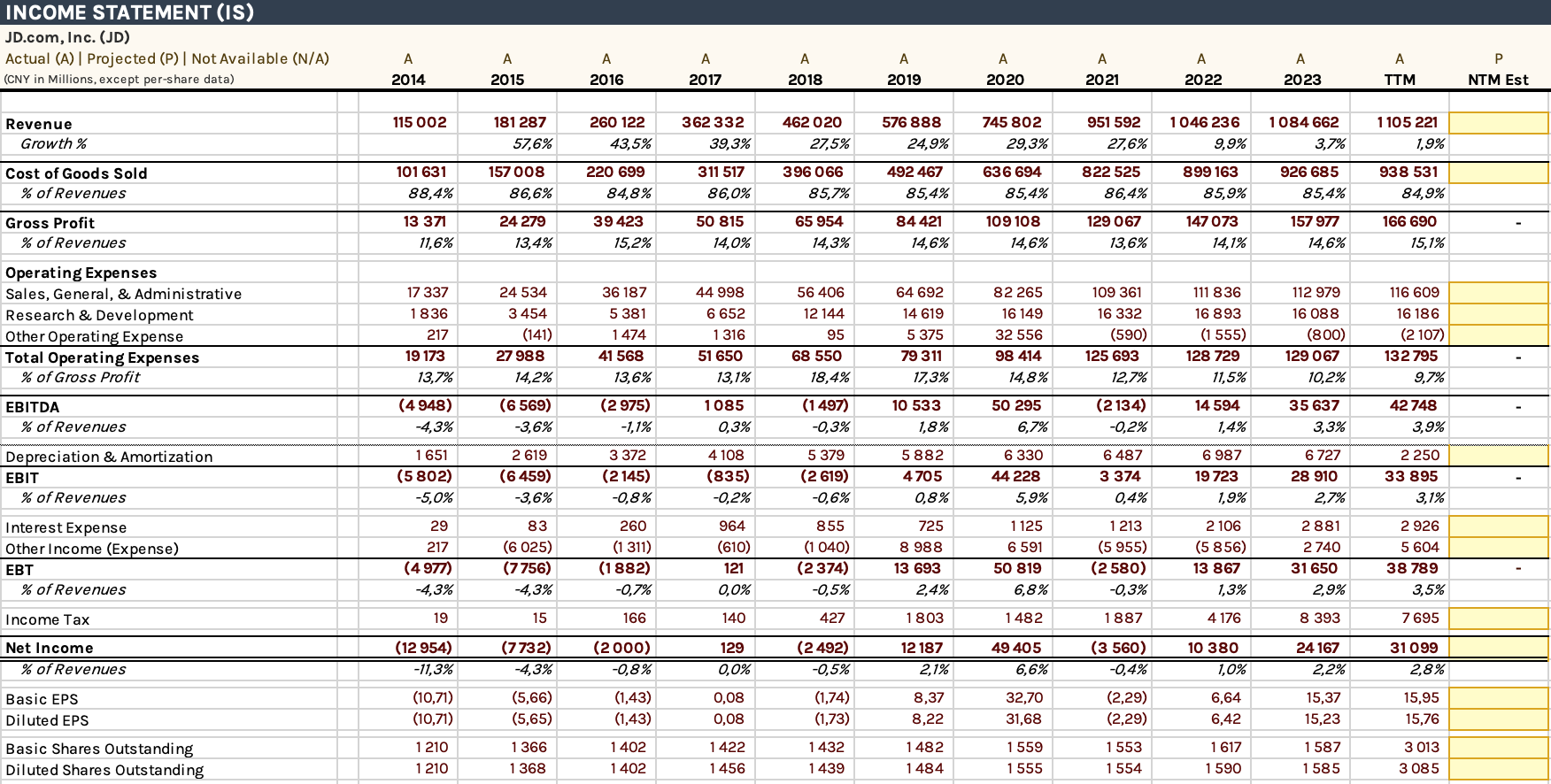

Income Statement

Revenue: JD have had great revenue growth until 2022 but have stagnated. The reason is weaker macroeconomics in China, a weakening yen which have led to Chinese shoppers purchasing goods from Japan, pricing war between E-commerce giants and problems with managing the Covid-19 pandemic. In tougher economic climates people tend to be more careful with their money and look for cheaper goods which disfavour premium retailers like JD and benefits companies that offer lower quality products at cheaper prices like Temu.

Gross margin: I mentioned in my first post “Introduction to Value Investing“ that a gross margin under 20% may be a indicator that the market is saturated and competitive. In this situation that is not the case. Most of JD’s revenue comes from selling goods directly to consumers which is more costly than connecting suppliers with customers similar to competition like Temu. JD have to have their own warehouses where they store inventory and a logistic network to ship them. Even though it is more expensive, it gives them more operational control over product quality and shipping time. The trends shows that JD is able to decrease the Cost of Goods Sold effectively. In summary, JD operates a capital heavy business model and as a consequence they operate on thinner margins than their competition. It lies within their strategy to be able to offer better product quality than competitors and faster shipping times.

SG&A / Gross Profit: Consistently around 70% which is in the higher quartile and indicate a competitive advantage. Around 350 000 people out of 500 000 work as in-house delivery personnel.

R&D: Around 10% of gross profit. Have not rapidly been increasing nor decreasing. Looks like it is stabilising almost like a fixed expense.

Depreciation: Very low and stable which is good.

Interest to operating income: 9% compared to Alibaba 15%, Pinduoduo 0.2%, Amazon 3%.

Net income: Profitable and a clear upward trend. Increasing as a percentage during the last 3 years despite slow revenue growth which indicates that they have been successful in getting rid of businesses bleeding cash which management communicated in their 2020 annual report. They have improved their business model and reduced cost showing integrity for management.

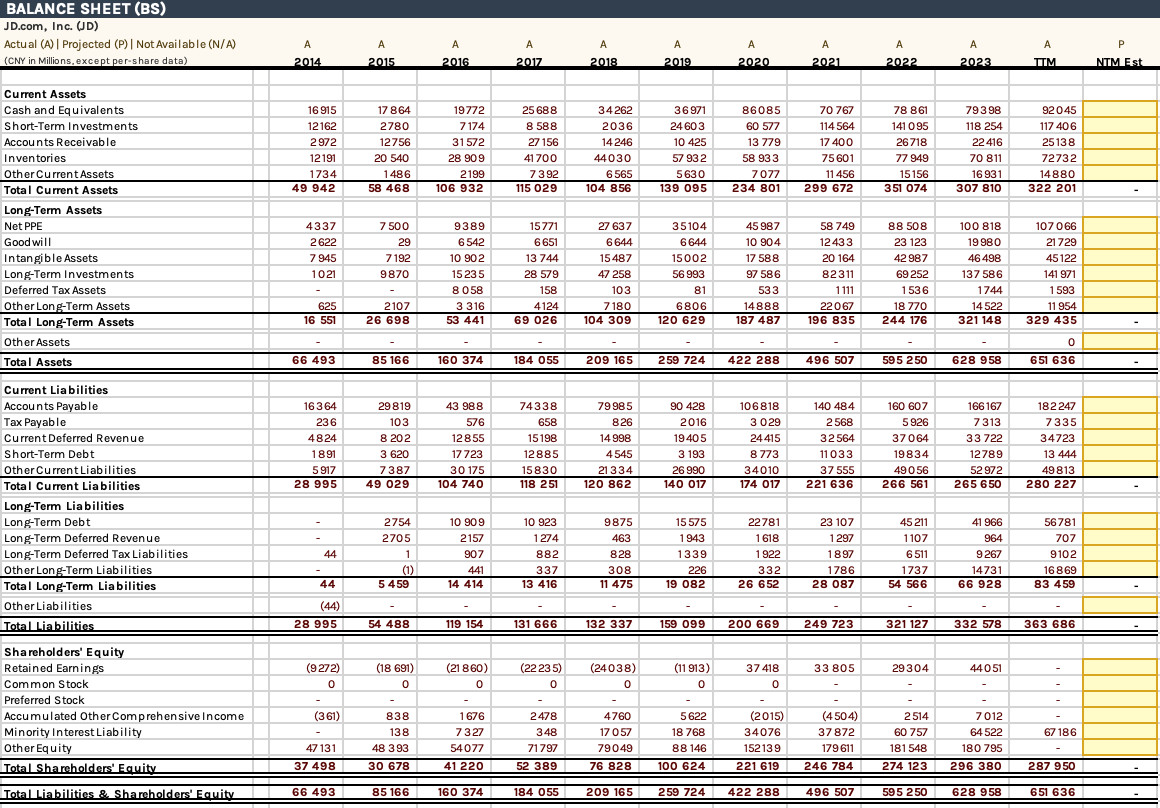

Balance sheet

Cash and Equivalents is rising which is good. Cash per share in US dollars (including short-term investments) is $21.11 compared to the share price today which is trading at $26.24. Net cash position after accounting for all debt is $10.88 per share. Parallel rise in inventory and net income. There are no surprises here either. Current ratio is over 1 which means they will meet their short-term obligations without any problems. PP&E is financed internally without the need of debt. Goodwill is not increasing massively which indicate that they don’t make many acquisitions and is focusing on their core businesses. JD would be able to pay off all their debt with their cash, equivalents and short-term investments or with 2 years of earnings. Debt to equity is 0.4. Retained earnings are piling up which is good. They have not issued any common or preferred stocks and they have begun purchasing back shares in accordance with their share repurchase program. The company may repurchase up to US$5.0 billion worth of its shares (including ADSs) over the next 36 months through the end of August 2027. The balance sheet is very healthy and there are no signs of financial problems. What I find most interesting regarding JD’s balance sheet is their net present value and liquidation value which is very close to the share price. Cash, equivalents and short term investment totaled $28.8 billion as of June 30, 2024. Account receivables is $2.978 billion, Inventory is $9.721 billion, other current assets is $1.916 Billion, PP&E is $10.758 billion, Land is $5.289, Equity Investments is $7.572 billion and Long-term investments is $11.964 Billion. The value of the aforementioned is in total $78.998 billion. After subtracting total liabilities which is $50.044, we get $28.954 Billion in net asset value which equals $18.80 per share or 72% of the current share price ($26.24). The idea is not to hope that JD will liquidate all their assets and stop operating, but rather get an insight to how big the margin of safety is. Free cash flow as of June 30, 2024 for TTM is $7.656 Billion which is $4.97 per share. Assuming that the free cash flow will not grow in the future it would take you 1.5 years to get back your investment in assets (excluding intangible assets and goodwill etc) and free cash flow. (Share price - Net Asset Value) / FCF = ($26.24 - $18.80 = $7.44 ⇒ $7.44 / $4.97 = 1.50). If we account for a discount rate of 10% (WACC) it would take just under 2 years.

Cash Flow Statement

Capital expenditure: Was $2.443 billion which high, net income was $4.311. The reason is that their PP&E requires a lot of capital investments.

Free Cash Flow: Free cash flow yield is 19.16% compared to Amazon’S 2.6% and Alibaba with 13%. There is also a clear upward trend despite slow revenue growth which means they are cutting cost and making their operations more efficient.

Growth Drivers and Market

China’s e-commerce market is the largest in the world, valued at approximately $3 trillion in 2023, and is projected to grow at a compound annual growth rate (CAGR) of 12% through 2027. JD.com, as one of the market leaders, has consistently outpaced the broader market. JD.com’s market share in China’s e-commerce sector is around 15%, making it the second-largest player after Alibaba. The company’s competitive advantages, such as its direct sales model, efficient logistics network, and a strong emphasis on product authenticity and quality, position it well to continue capturing a significant share of the growing market. Additionally, JD.com’s expansion into lower-tier cities, which still have relatively low e-commerce penetration rates, represents a substantial growth opportunity as these regions are expected to see accelerated online shopping adoption in the coming years. China is moving towards a middle income country where more people are getting dragged out of poverty which will benefit premium retailer JD as customers will priorities higher quality goods over cheaper ones. During the economic slowdown in China JD have made their business more effective by cutting cost and getting rid of businesses that were losing money. The E-commerce market in China is expected to growth 9.95% per year between 2024-2029 and user penetration will be 78.8% in 2024 and is expected to hit 97.4% by 2029. This means that JD.com will likely grow their business without having to take market shares from competitors. They are also opening up warehouses in Europe to enable Chinese sellers to easily sell to European customers with low shipping times.

Summary

I will never try to forecast what will happen in the future. I simply try to answer the following 4 questions: How much will I make? When will I make it? How sure am I? How much do I lose if I’m wrong?

My rationale behind my thesis is that if I have misunderstood, misinterpreted or simply made a wrongful analysis about JD’s position in the Chinese E-commerce market, I will not lose huge amounts of money. On the other side, if I’m correct I believe there will be more than an adequate return to be made. In an ideal scenario, JD will both be able to expand their market share in a growing market, while continuing to cutting expenses and expanding to Europe. If the latter scenario were to appear, JD will grow faster than the overall market growth of 9.95%. If you purchased a bond with a yield of 20% and a growth rate of over 10% a year, you would do pretty good on your investment compared to the overall market in the long-term.

Thanks for reading,

Philip Åström

---

Feel free to ask questions or provide feedback in the comments below, and if you find value in this, don’t forget to subscribe for more updates, it’s free!